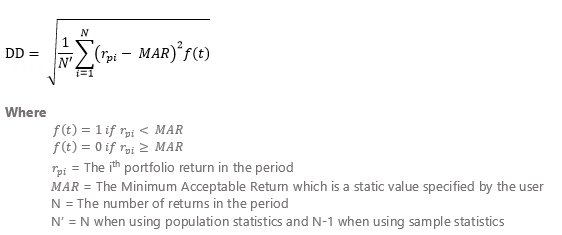

A measure of downside risk that focuses on returns that fall below a minimum threshold or minimum acceptable return (MAR). It is used in the calculation of a risk measure known as the Sortino Ratio.

The Calculation

To find out if your firm is using population or sample statistics, please contact your dedicated service team.

When Downside Deviation Uses Gross or Net Returns

On the Account Analytics report, you can control whether this calculation uses net or gross with Show Returns As (Net or Gross).

When you run composites, the Composite Statistics report reports only on gross returns. For more information, see Composite Statistics.